Tax does not add a layer; it changes the system

This is not rhetorical provocation. It is an architectural observation. When a tax authority mandates real-time invoice transmission, structured XML format, digital signature, globally unique numbering, and five-year onshore storage — as the UAE Federal Tax Authority now does under Ministerial Decisions 243 and 244 of 2025 — every one of those requirements rewrites a system decision that was previously made without compliance in view.

The invoice numbering schema changes. The data model expands. The output format shifts from a PDF rendered by a document module to a structured PINT AE XML payload transmitted via API to an accredited service provider. The audit trail, previously an afterthought, becomes a primary system function. None of this is configuration. It is redesign — and the organisations that understand this distinction early will absorb it as a planned architectural evolution rather than an emergency remediation programme.

The UAE Regulatory Stack: What the Architecture Must Now Support

Understanding the architectural impact of UAE tax compliance requires mapping the regulatory stack that the ERP must now execute against — not abstractly, but as a set of concrete system requirements.

Federal Decree-Law No. 8 of 2017 introduced VAT at 5% across most categories of goods and services. This established the baseline system requirements: transaction-level tax classification, compliant invoice generation, period VAT returns filed with the FTA, and audit-ready record maintenance for a minimum of five years under Federal Law No. 7 of 2017. ERP systems implemented before or during the 2018 VAT launch were designed to meet these requirements — in many cases through localisation modules, manual field additions, and PDF invoice templates.

Cabinet Decision No. 109 of 2023 changed the architecture problem fundamentally. It established the legal basis for mandatory e-invoicing in the UAE, initiating a programme that Ministerial Decisions 243 and 244 of 2025 have since operationalised with specific technical and business requirements.

From 31 July 2026, all businesses with AED 50 million or more in annual revenue must issue compliant e-invoices in the PINT AE structured format. From 1 January 2027, the mandate extends to all remaining VAT-registered entities.

The PINT AE data model defines mandatory and optional fields for UAE e-invoices, tax credit notes, and related documents — a standard designed to improve VAT compliance, transparency, and auditability across the system.

The system requirements this introduces are not incremental to the VAT requirements already in place. They are structurally different. An ERP that cannot generate XML-formatted invoices without a third-party add-on, or whose invoice numbering is sequential within each financial year rather than globally unique across the full life of the business's VAT registration, is structurally non-compliant — and cannot be made compliant through configuration alone.

For CIOs and CTOs, this is the diagnostic question: does your current ERP architecture produce PINT AE XML, transmit via API to an FTA-accredited service provider, enforce globally unique sequential invoice numbering, apply digital signatures, and maintain timestamped audit records in on-shore storage? If the answer to any of those questions is no, the gap is architectural.

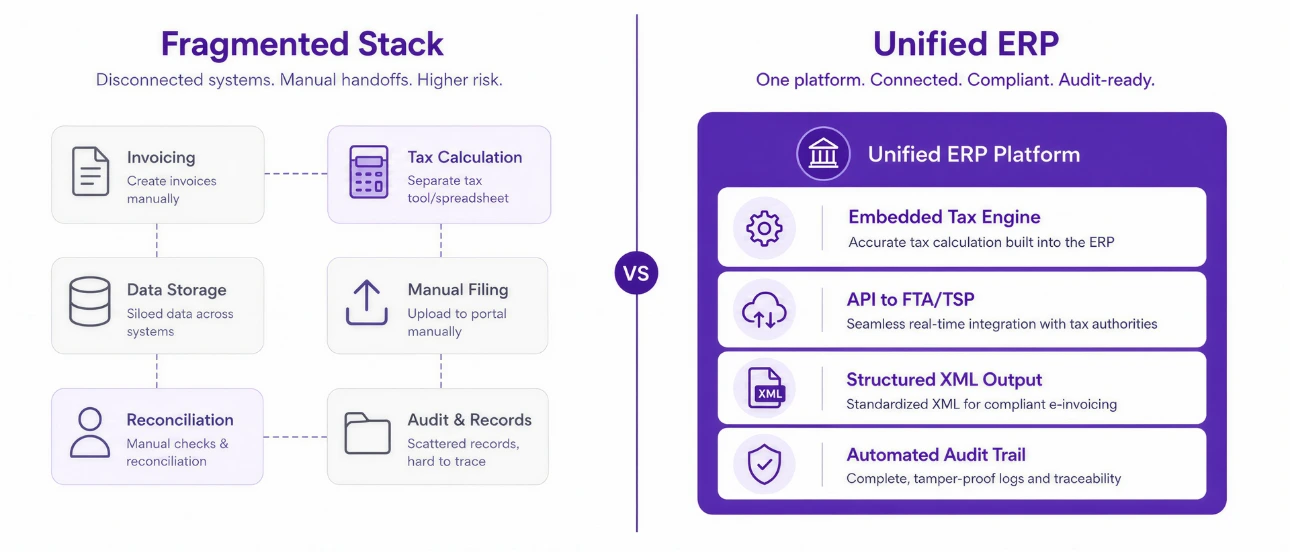

Fragmentation: The Hidden Cost of Compliance-as-Patch

The most dangerous pattern in enterprise tax compliance architecture is not non-compliance at a point in time. It is the accumulation of compliance patches that produce fragmentation over time — a system that meets each regulatory requirement individually but loses architectural coherence in the process.

Fragmented compliance stacks create vendor sprawl, integration strain, and operational inefficiencies. Once indirect tax, e-invoicing, and global trade compliance are added across multiple jurisdictions, APIs multiply, regulatory updates arrive on different schedules, and vendor overlap introduces hidden cost and risk.

In multi-entity GCC organisations, this fragmentation follows a recognisable pattern. The ERP was implemented with a localisation module for UAE VAT. A separate tool was procured for VAT return preparation. A PDF invoice template was customised to include mandatory fields. Each intervention addressed a specific compliance requirement at the time it was introduced. Collectively, they produced an architecture where tax logic is distributed across multiple systems, maintained by different teams, and updated on different schedules.

The consequence is not merely operational inefficiency. It is a structural audit risk. Late-stage tax integration can derail ERP transformation timelines, inflate costs, and elevate compliance risk — and this is precisely what fragmented architectures produce when a new mandate arrives: a remediation programme that is more expensive and more disruptive than a planned architectural redesign would have been.

Multi-jurisdiction tax compliance demands integrated solutions that connect calculation, e-invoicing, filing, and reporting workflows within a unified system architecture. Organisations expanding across borders face fragmented systems, manual obligation tracking, and regulatory change velocity that manual processes cannot match.

For a CTO reviewing the current state of a multi-entity organisation's tax architecture, the relevant diagnostic is not whether the system is currently compliant. It is whether the architecture can absorb the next regulatory change — the e-invoicing mandate, the CTC framework evolution, or the next amendment to the VAT Executive Regulations — without triggering another round of fragmentation.

This is directly connected to the pattern described in GCC operating model fragmentation: regulatory pressure applied to a fragmented system does not produce compliance — it produces deeper fragmentation.

How Tax Requirements Rewrite Three Core System Layers

Regulatory compliance in the UAE's current environment does not map to a single system module. It imposes requirements across three distinct architectural layers, each of which must be addressed as part of a coherent design rather than patched independently.

Layer 1: The Transaction Data Model

The PINT AE standard specifies the data structure of every compliant invoice. Mandatory fields include supplier and buyer tax identification numbers, business registration details, unique invoice identification, tax classification per line item, and the specific treatment of exempt and zero-rated supplies.

For ERP systems, this means the transaction data model must capture these fields at the point of transaction creation — not at the point of invoice generation. The distinction matters because data not captured at the transaction level cannot be reliably reconstructed at the invoice level. Organisations that have treated VAT classification as an invoice rendering problem, rather than a transaction recording problem, will find their data model incompatible with PINT AE requirements.

PwC's tax ERP practice identifies this directly: tax-sensitive ERP design requires tax-sensitising the general ledger to meet transactional processing requirements, evaluating fixed asset master data to support property and income tax requirements, and incorporating transfer pricing considerations into intercompany transaction processing at the data model level (PwC, Tax Enterprise Resource Planning Services). This is not an invoice formatting exercise. It is a data architecture exercise.

Layer 2: Transaction Validation Logic

The e-invoicing framework introduces validation requirements that must execute at the point of transaction creation, not at the point of FTA submission. Compliance requires that invoices are generated in structured digital format, pass compliance checks before submission, are transmitted securely to authorised platforms, and are stored electronically for audit and legal requirements.

The architectural implication is clear: validation logic — tax code verification, TRN validation, mandatory field completeness, classification consistency — must be embedded in the ERP's transaction processing layer, not in a downstream reporting or submission module. An invoice that fails FTA validation after submission creates an audit event. An invoice validated before creation does not.

The market preference has shifted decisively toward tightly coupled, system-level tax functionality: native integration replacing workaround-driven compliance, embedded tax engines, standardised APIs, and real-time data exchange. For CIOs evaluating their current architecture, the question is whether validation is embedded or bolted on — and whether it executes before or after the transaction record is created.

Layer 3: Reporting and Audit Architecture

UAE e-invoicing under the PEPPOL 5-corner model requires that invoice data be transmitted to an accredited service provider (ASP) connected to the FTA's electronic exchange network (EEN). This transmission must occur at invoice creation — not at period end. The FTA receives a real-time data feed of every compliant invoice issued by every in-scope business.

For the ERP, this means reporting architecture shifts from a periodic batch activity to a continuous transactional one. The system must maintain API connectivity to the ASP, handle transmission errors and resubmissions at the transaction level, and maintain an audit trail that records not only invoice content but the transmission event, the FTA response, and the archive timestamp.

Cloud ERP platforms hold a structural advantage here: they handle high transaction volumes without infrastructure upgrades, support instant invoice validation and reporting, stay aligned with regulatory changes, and enable seamless communication with government portals through built-in encryption and access controls. This is the architectural case for cloud alignment in UAE tax compliance — not as a modernisation preference, but as a functional requirement imposed by the e-invoicing framework itself.

Cloud Alignment as a Structural Response to Regulatory Velocity

The e-invoicing mandate is not a static requirement. The UAE's framework, modelled in part on Saudi Arabia's ZATCA implementation, is designed to evolve — from a reporting model toward a clearance model, where the FTA validates invoices before they are legally issued rather than after. This regulatory trajectory means architecture must be built not only for the current mandate but for the compliance requirements that will follow it.

On-premise ERP systems face a structural disadvantage in this environment. Each regulatory update to the PINT AE data model, the FTA's API specifications, or the ASP connectivity requirements triggers a local implementation project — with the associated cost, testing cycle, and business disruption that implies, each time the framework evolves. In a cloud deployment, this update is managed and distributed by the platform vendor.

The Thomson Reuters indirect tax practice frames the CIO and CTO mandate clearly: partner early with ERP leadership and enterprise architecture; map tax-sensitive data, legal entities, and jurisdictional requirements to systems; define e-invoicing and continuous transaction control requirements market by market; and ensure APIs, data models, and workflows are designed for continuous reporting (Thomson Reuters, October 2025). This is an architectural design instruction, not a compliance checklist.

For multi-entity organisations operating across UAE mainland entities, free zones, and other GCC jurisdictions, cloud alignment provides a unified compliance architecture that accommodates entity-level differences — different TRNs, different ASP configurations, different invoice types — within a consistent structural framework. This is precisely the technology alignment with operating model design challenge that multi-entity enterprises face: entity-level variation in regulatory profile, managed within a unified system architecture rather than through parallel systems.

A Redesign Pattern: From Fragmentation to Consistency

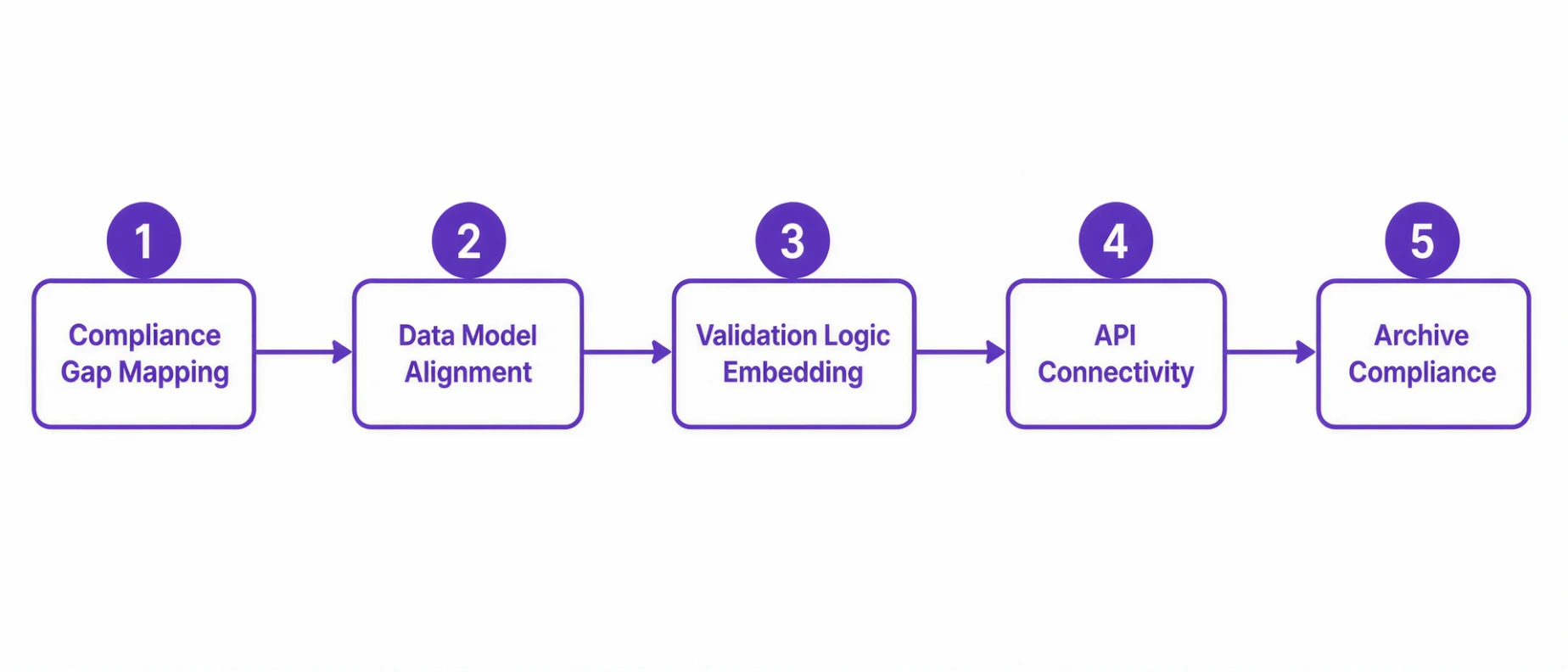

The path from a fragmented compliance architecture to a consistent one follows a specific sequence. Understanding this sequence allows CIOs and CTOs to scope the redesign accurately — distinguishing between what requires architectural change and what can be resolved through configuration.

Step one: Compliance gap mapping at the system layer

Map every requirement introduced by the PINT AE standard, the e-invoicing mandate, and current FTA administrative guidance against the existing system architecture. For each requirement, identify whether it is met through the ERP's core data model and validation logic, through a downstream module or external tool, or through a manual process. This produces a map of architectural gaps — requirements the system cannot meet structurally rather than operationally.

Step two: Data model alignment

Redesign the ERP's transaction data model to capture all PINT AE-required fields at the point of transaction creation. This includes tax classification at line-item level, TRN fields for both supplier and buyer, globally unique invoice numbering across all entities, and treatment fields for exempt, zero-rated, and standard-rated supplies. Reporting and transmission architecture built on a non-compliant data model will fail under FTA scrutiny regardless of how well the output layer is designed.

Step three: Validation logic embedding

Move tax validation from the invoice generation or submission module into the transaction creation workflow. Define validation rules that enforce PINT AE field completeness, tax code consistency, and TRN format before the transaction record is committed. Build error handling that surfaces validation failures at the transaction level, not at the FTA submission level.

Step four: API connectivity and transmission architecture

Design the API layer that connects the ERP to the accredited service provider covering invoice transmission events, error handling and resubmission logic, FTA response capture, and transaction-level audit trail records. For multi-entity organisations, this layer must support entity-specific ASP configurations within a unified audit architecture.

Step five: Archive and retention compliance

UAE regulations require electronic archiving of compliant invoices for a minimum of five years, with digital signatures, timestamps, and secure on-shore storage built into the system from the outset. Audit requests must be fulfillable directly from the system not through manual document retrieval.

Organisations that executed this sequence before the mandate deadline report not only compliance achievement but operational improvement: smoother integration with key buyers, no emergency implementation costs, and commercial relationships strengthened rather than strained. The preparation timeline is the determining factor. Organisations that engaged their ERP vendor and ASP in advance completed the transition within standard project cycles. Those that delayed faced remediation timelines and remediation costs that a planned redesign would have avoided entirely.

This is exactly what Odoo ERP implementation and consulting in the UAE context requires: compliance requirements mapped to system architecture before implementation begins, not layered onto a system designed without them.

The Governance Layer: Sustaining Compliance Architecture Over Time

Achieving compliance at the mandate deadline is a milestone. Sustaining it as the regulatory framework evolves is an ongoing architectural discipline. The PINT AE data model will be updated. The FTA's API specifications will be revised. The regulatory scope will expand. An architecture that was compliant at go-live but cannot absorb these changes without emergency remediation is not a compliance architecture. It is a compliance event.

Sustained compliance architecture requires governance at three levels. At the system level: a change management process that translates regulatory updates into system change requests, evaluates their impact on the data model and validation logic, and executes changes within a controlled release cycle. At the operations level: monitoring of FTA transmission responses, error rates, and rejection patterns that surface compliance issues before they accumulate into audit risk. At the entity level: compliance review processes for each legal entity, accounting for the different regulatory profiles of mainland, free zone, and branch structures within the group.

This governance discipline is what governance sustains system value in enterprise environments describes at the strategic level: architecture delivers value not at the point of implementation, but over the governance lifecycle that follows it.

Advisory note: The regulatory references in this post reflect publicly available FTA, Ministry of Finance, and UAE government documentation as of the date of publication. Specific compliance timelines, thresholds, and technical specifications are subject to regulatory update. Organisations should validate all compliance interpretations with qualified legal and tax advisors before making implementation or architectural decisions.

Strategic Takeaway: Architecture Is the Risk Management Decision

For a CIO or CTO in a UAE multi-entity enterprise, the e-invoicing mandate is not a compliance department problem. It is a system architecture problem that the compliance department will surface at the worst possible moment — at the point of enforcement — if it is not resolved through planned architectural redesign now.

Tax requirements in the UAE do not add a compliance layer to an existing ERP. They change the transaction data model. They change the validation logic. They change the output format. They change the transmission architecture. They change the retention and audit framework. The organisations that treat these as additive requirements — patching each one onto an architecture not designed to accommodate them — will produce fragmented, expensive, and brittle compliance systems that deteriorate with every subsequent regulatory update.

The organisations that redesign the architecture once, correctly, with the full regulatory stack in view, will achieve something more valuable than compliance: an ERP structurally ready for the regulatory environment it will operate in for the next decade.

The investment is the same either way. The difference is whether it is made by design or by crisis.

Related Insights

- Industry-Specific ERP Systems: How UAE Regulations Shape Architecture

- GCC Operating Model Fragmentation and System Consequences

- Technology Alignment with Operating Model Design

- Governance Sustains System Value in Enterprise Environments

- Multi-Entity Process Design and Execution Complexity

Frequently asked questions

The FTA's mandate under Ministerial Decisions 243 and 244 of 2025 requires ERP systems to generate invoices in PINT AE XML format, enforce globally unique sequential invoice numbering across the full VAT registration lifecycle, apply digital signatures, transmit invoices via API to an FTA-accredited service provider at the point of issuance, and archive records on-shore for a minimum of five years. These requirements cannot be met by configuring an existing PDF invoice template — they require changes to the data model, validation logic, and output architecture.

Configuration adjusts system behaviour within its designed parameters — changing a tax rate, adding a field, modifying a template. Architecture changes the system's structure — how data is captured, how transactions are validated, how outputs are generated, how records are transmitted and stored. UAE e-invoicing requirements affect all four dimensions. A system whose data model does not capture PINT AE fields at the transaction level, or whose validation logic runs after the transaction record is committed, cannot be made compliant through configuration. The structure itself must change.

Each in-scope legal entity requires its own compliant invoicing architecture — its own Tax Registration Number, its own accredited service provider configuration, and its own invoice series. The data model must capture entity context at the transaction level. The API transmission layer must route each invoice to the correct entity's ASP. The audit architecture must maintain entity-level records presentable to the FTA independently for each entity. Organisations built on a single-entity ERP model must redesign the entity layer explicitly as part of their e-invoicing programme.

The UAE's e-invoicing framework will continue to evolve — data model updates, API specification changes, and the potential shift toward a clearance model will each require system updates. Cloud ERP platforms deliver these through the vendor's release cycle, without a local implementation project each time. On-premise deployments require a local update for every regulatory revision — with the associated cost, testing, and disruption that implies. For a framework designed to evolve, cloud deployment is a structural advantage, not a preference.

The mandatory compliance date for businesses with AED 50 million or more in annual revenue is 31 July 2026. ERP-level architectural changes — data model redesign, validation logic embedding, API connectivity to a certified ASP, and archive configuration — typically require six to twelve months as planned projects. Organisations that begin after February 2026 face material risk of either missing the deadline or incurring significantly higher emergency implementation costs. Early engagement produces compliance on budget and on schedule. Late engagement produces crisis remediation.